Why Robinhood Banned Box Spreads

Arbitrage Bounds on European Options. Perpetuals and Smooth Pasting Conditions. Free Boundary Problems. The Greeks for American Options.

This post will be more technical and mathematically involved than most of what I’ve written, but some of the results should be very satisfying. Feel free to skip the math though if you are not into that; if you are into the math make sure you’ve check out my previous post on the intuition in the Black-Scholes model or at least have a basic understanding of it.

I am also not smart enough to have come up with some of the more technical aspects of this post, and will cite sources in the article to give credit where it is due. Some of the reference texts used are Paul Wilmott on Quantitative Finance by Paul Wilmott and Option Volatility and Pricing by Sheldon Natenberg.

The Legend Of u/1R0NYMAN

For this section, I am just going to quote the MarketWatch article:

Investing legend Jack Bogle once said that “if you have trouble imagining a 20% loss in the stock market, you shouldn’t be in stocks.” He didn’t mention anything about a 2,000% loss though. That’s where 1R0NYMAN comes in. The anonymous trader/internet hero created a stir on Reddit earlier this month with this absolute corker of a trade

It’s called a box spread, a four-sided options strategy billed, in theory, as a riskless arbitrage play using call and put options. In this case, it started with a $5,000 “investment” executed through Robinhood, a no-commission trading platform. Clearly, 1R0NYMAN figured it was a slam dunk. “I have no money at risk,” he responded to those questioning his approach in Reddit’s raucous “Wall Street Bets” group:

“It literally cannot go tits up.”

Famous last words.

Even one of the group’s moderators pleaded, “DO NOT DO THIS,” pointing out the potential downside. But that didn’t stop 1R0NYMAN. In fact, he apparently managed to withdraw $10,000 before it all hit the fan. And hit the fan it did. A few days and some unforeseen twists later, he shared the results:

Robinhood, the investing app that came under fire for the clumsy rollout of its cash management accounts last month, decided soon after that it would no longer allow the trading of box spreads. “A box spread is an options strategy created by opening a call spread and a put spread with the same strike prices and expiration dates,” Robinhood wrote. “Box spreads are often mistaken for an arbitrage opportunity, however, they have hidden risks that could lead to losing much more money than expected.”

The short version of the story is that the box spread would have been risk-free if they were made of European-style options that could not be early exercised. However, American-style options can be, and in this case, were exercised early. For the rest of the post, we will dive into why 1R0NYMAN’s counterparties would have early exercises their American-style options, and explore some of math and implications for early exercise in general along the way.

The Arbitrage Bounds for European Options (Natenberg)

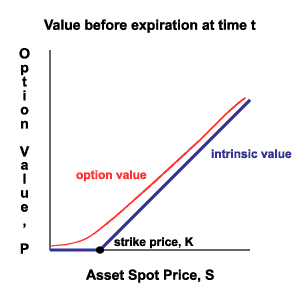

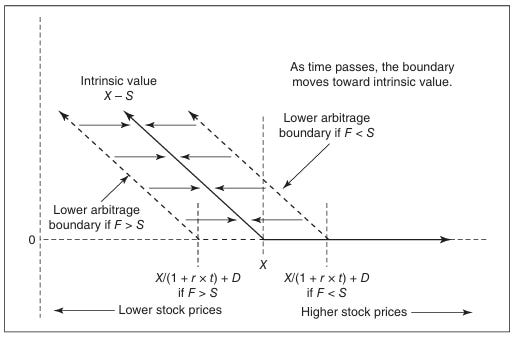

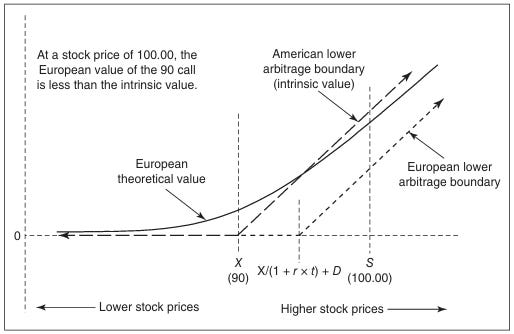

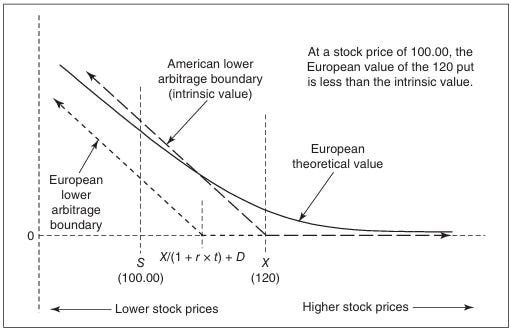

Most textbooks and classes use a graph like the one below to demonstrate the option time / optionality value before expiration by drawing a smooth line for the option value strictly above the intrinsic value. However, is this picture always accurate?

To examine the accuracy of the above picture, we need to carefully consider the actual no-arbitrage condition for options. If the option is American, then it can be exercised at any point and indeed the option cannot fall below its intrinsic value. As such, the option value is at least equal (not not necessarily strictly above), its intrinsic value.

We now consider the case of a European call option, via put-call parity static replication we can write

where C is the call value, P is the put value, S is the underlying value, and X is the strike. However, we know that the put value is at least 0 so in fact we can write

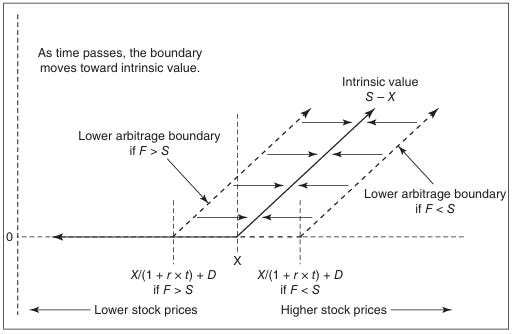

This shows that under the assumption of no dividends and non-negative interest rates, the call value is always greater than the value of immediate exercise, and as such it is never optimal to exercise the call early. However, let us now stretch these assumptions and add a dividend term, the lower arbitrage bound is now

where D is the dividend. Moreover, for underlying that are not stocks, other costs and benefits of carry should also be added into the arbitrage consideration. Depending on if the forward price F is greater or less than the spot price S, the lower arbitrage boundary is presented below (graphic from Natenberg figure 16-3):

A similar analysis can also give us the arbitrage bounds for puts

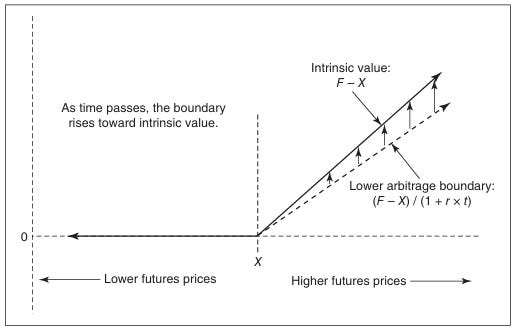

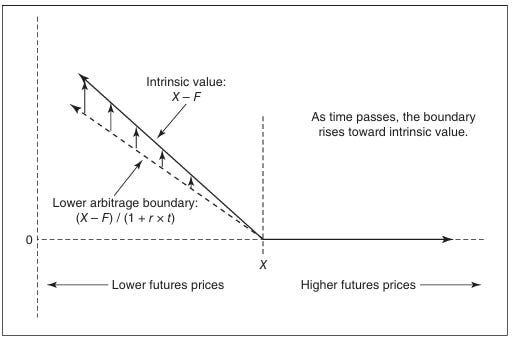

What if the option was on futures instead of spot? This allows us to discount the effects of dividends as well as any of the benefits and costs of carry. However, rates still matter. The graph changes to the following:

A similar analysis can also give us the arbitrage bounds for puts

Early Exercise of American Options (Natenberg)

Under what conditions might we choose to exercise an American call option early? We can answer this question by considering the value components of a call

Call value = intrinsic value + volatility value + interest value – dividend value

Suppose that we find

Dividend value > volatility value + interest value

In this case, the value of the call will be less than intrinsic value. How do we decide when to exercise? For a call option on stock, the only day on which a trader need consider early exercise is clearly the day before the stock pays a dividend (what about multiple dividends in LEAPS, we will get to that later). It is also worthy to note that the conditions under which an American option becomes an early exercise candidate are also equivalent to the conditions under which a European call option gains both positive theta and gamma (since option price moves towards intrinsic over time).

Under what conditions might we choose to exercise an American put option early? We consider the value of the put in a decomposition

Put value = intrinsic value + volatility value – interest value + dividend value

Suppose that we find

Interest value > volatility value + dividend value

In this case, the value of the put will be less than intrinsic value. When should we exercise a put early? The most common day on which to exercise a stock option put early is the day on which the stock pays the dividend. However, an even earlier date may be reasonable if interest value is high enough.

Early Exercise of American Options (Wilmott)

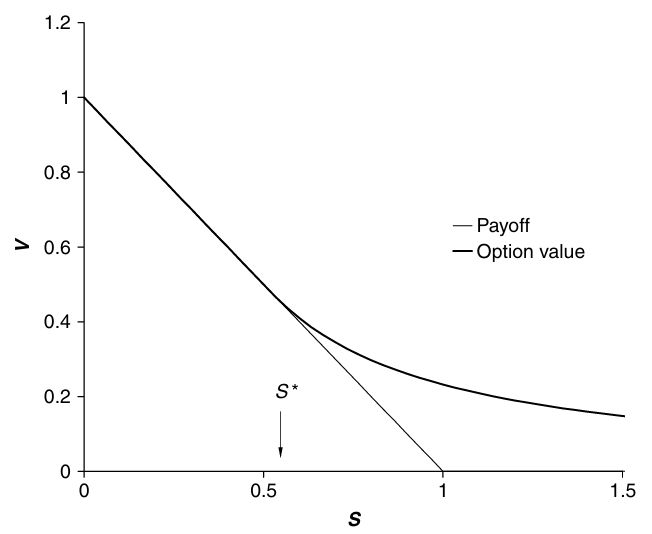

For readers who are more mathematically inclined, the above explanation may not prove too satisfying. We will now give a more technical explanation for the conditions of early exercise. Consider the example of a perpetual American put can be exercised for a put payoff at any time with no expiry.

The option value V would be independent of time since by definition it is perpetual i.e. it would have no theta. In addition, by no-arbitrage it cannot go below its intrinsic value. Lastly, we note that that when value of the option is strictly greater than the payoff, it must satisfy the Black–Scholes equation less the theta term (using the same dynamic hedging argument in the original equation) i.e. the perpetual satisfies

This is a linear, homogeneous, second-order ODE. It has general solution in the form

for arbitrary constants A and B. Note that the two parts of the solution are themselves solution to the ODE (by linearity of the ODE).

The first part of the solution (AS) is interpretable as the underlying itself; the underlying itself trivially satisfies the tweaked version of the Black-Scholes ODE. However, in describing the perpetual put, it’s clear that A must be 0 since as S tends towards infinity the value of the option itself must go to 0. So really we have

Now we turn to B. Note that at some point when the asset is in the money we want to exercise it, paying exercise price E and receiving E − S. Suppose S = S* is the exercise value, what are some equations that we can now write down? First, When S=S* the option value we must be indifferent to holding the option versus exercise i.e.

Now, we can use the equation for V(S) and the equation for V(S*) to eliminate B

We want to choose S* to maximize the option’s value at any time before exercise. We find this by differentiating the above with respect to S*.

Setting the above to 0, we find that the optimal S* is given by

This choice maximizes V(S) for all S ≥ S*. With this S*, we can uniquely determine B and therefore determine the value of the option prior to exercise.

From looking at the above graph, the observant reader will notice that the slope of the option value and the slope of the payoff function are the same at S = S*. To prove this, we can examine the difference between the option value and the payoff function

Differentiating this with respect to S and we will find that the expression is zero at the point of optimal exercise. In other words, assuming continuous interests and dividends (yield on foreign currency, for example), we ought to exercise the option as soon as the asset price reaches the level at which the option price and the payoff meet. Another equivalent statement is that the American option value is maximized by an exercise strategy that makes the option value and option delta continuous i.e. solving the Black–Scholes equation with continuity of option value and option delta. This is called the high-contact or smooth-pasting condition.

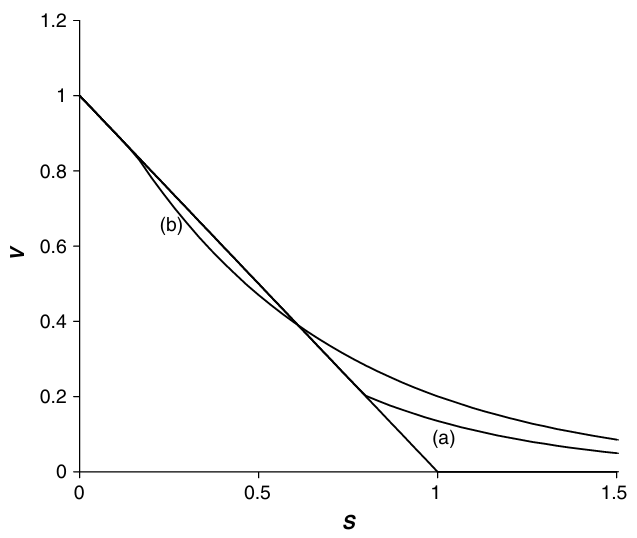

Another way of looking at the condition of continuity of delta is to consider what happens if the delta is not continuous at the exercise point. The two possibilities are shown in below and curve (a) corresponds to exercise that is not optimal because it is too early while in (b) there is clearly an arbitrage opportunity i.e. exercise is too late.

For completeness we now present the valuation of the perpetual call and puts when there is a continuously paid and constant dividend yield or benefit of carry on the asset. The relevant ordinary differential equation for the perpetual option is

The general solution is

where

with a- < 0 < a+. The perpetual put has value

where

and the optimal exercise value

The perpetual call has value

where

and optimal exercise value

Note when D = 0, V = S and S∗ tends toward infinity. This again shows that it is never optimal to exercise the American call when there are no dividends on the underlying.

The Free Boundary Problem for American Options (Wilmott)

Can we determined the closed-form solutions for the exercise of American options that are not perpetual? The answer is that no one has yet been able to do so. In this section I give an overview of the difficulty in this problem. Recall that in the Black–Scholes argument for European options the theta and gamma balance out to produce the risk-free rate in a delta-hedged portfolio of option and stock; however, the writer of the American option can make more than the risk-free rate if the holder does not exercise optimally. As such, the Black–Scholes Equation becomes an inequality

Moreover, Black–Scholes argument only applies to cases where the underlying is not in a place where early exercise is optimal. If early exercise is optimal, then the value of the option comes not from delta-hedging but rather from actually exercising the option. We now consider the boundary conditions . For an early exercise payoff of P(S,t), we know that the value of the option V(S,t) must satisfy

at expiration

from previous, we know that the value is maximized if

The European Option satisfies two of the above constraints, but clearly not the one stating that the option value is always greater than or equal to the exercised value. As Wilmott puts it:

If the constraint is not satisfied somewhere then the problem has not been solved anywhere; i.e. due to the “diffusive” nature of the differential equation; an error in the solution at any point is immediately propagated everywhere.

The problem for the American option is known as a free boundary problem. In the European option problem we know that we must solve for all values of S from zero to infinity. When the option is American we do not know a priori where the Black–Scholes equation is to be satisfied; this must be found as part of the solution. This means that we do not know the position of the early exercise boundary. Moreover, except in special and trivial cases, this position is time-dependent. For example, we should exercise the American put if the asset value falls below S*(t), but how do we find S*(t)?

Not only is this problem much harder than the fixed boundary problem (for example, where we know that we solve for S between zero and infinity), but this also makes the problem non linear. That is, if we have two solutions of the problem we do not get another solution if we add them together. This is easily shown by considering the perpetual American straddle on a dividend-paying stock.

The reason that this contract is not the sum of two other American options is that there is only one exercise opportunity; the two-option contract has one exercise opportunity per contract. If the contracts were both European then the sum of the two separate solutions would give the correct answer; the European valuation problem is linear.

This contract can also be used to demonstrate that there can easily be more than one optimal exercise boundary. With the perpetual American straddle, as defined here, one should exercise either if the asset gets too low or too high. The exact positions of the boundaries can be determined by making the option and its delta everywhere continuous. One can imagine that if a contract has a really strange payoff, that there could be any number of free boundaries.

The Delta of American Options

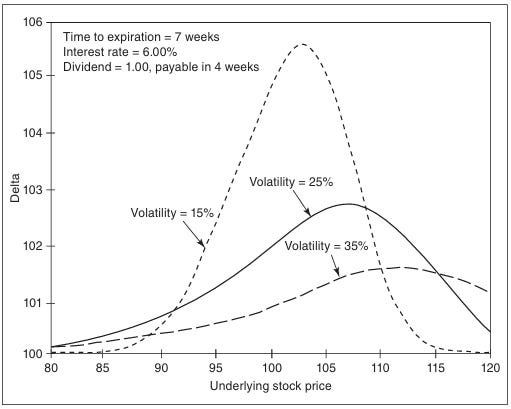

The delta (as well as other Greeks) of American options are affected by the probability of early exercise. This should be intuitive since at exercise, the Black-Scholes argument no longer applies to the option. Recall that we stated that an option is optimally exercised early when its theoretical value is exactly to parity, since it is touching the payoff diagram (i.e. intrinsic value) at this time, for a call option its delta is exactly 100 while for a put option its delta is exactly -100. This means that we an expect the delta of an American call to be higher than that of a European call, since the delta curve needs to be “lifted” so that it is 100 at the price of optimal exercise (dependent on time) instead of at infinity. The same analysis applies to puts.

The likelihood of early exercise will increase, and with it the difference between American and European values, as the option goes more deeply into the money. Moreover, at a higher volatility, the difference in values is smaller because the American call is less likely to be exercised early (more volatility value), and the reverse is true for lower volatility. The effect of time remaining till exercise is similar.

These dynamics can lead us to some interesting results. For example, a synthetic future (long call short put on same strike) done with European options will always have 100 delta. However, American synthetic futures can have delta higher than 100 since one of the legs can be exercised early (choice of strike doesn’t matter):

1R0NYMAN’s Box Spreads

A box spread is an options strategy that involves simultaneously buying and selling both calls and puts with different strike prices but the same expiration date. The strategy consists of buying a call and selling a put at a lower strike price, while selling a call and buying a put at a higher strike price. This combination creates a position with a guaranteed payoff at expiration, equal to the difference between the two strike prices, regardless of where the underlying asset's price ends up.

Buy a call option with a lower strike price (K1)

Sell a call option with a higher strike price (K2)

Buy a put option with a higher strike price (K2)

Sell a put option with a lower strike price (K1)

At expiration, regardless of where the underlying asset's price is, the payoff of a box spread is always the difference between the two strike prices (K2 - K1).

If the asset price (S) at expiration is below K1: Both puts are in-the-money (ITM), both calls are out-of-the-money (OTM). Payoff = (K2 - S) - (K1 - S) = K2 - K1.

If the asset price (S) is between K1 and K2: Lower strike call and higher strike put are ITM. Payoff = (S - K1) + (K2 - S) = K2 - K1.

If the asset price (S) is above K2: Both calls are in-the-money, both puts are out-of-the-money. Payoff = (S - K1) - (S - K2) = K2 - K1.

The box spread's fixed payoff (when done using European options) makes it equivalent to a zero-coupon bond, effectively allowing traders to lend or borrow at an implied interest rate. If you can set up the box spread for less than the present value of the payoff, you're essentially lending money at a higher rate than the risk-free rate. Conversely, if you can set it up for more than the present value of the payoff, you're borrowing at a lower rate. The difference between the cost of setting up the spread and the discounted value of the payoff represents the implied interest.

For example, if the strikes are $50 and $60, the payoff will always be $10 at expiration. If you can set up this spread for $9.50 with one year to expiration, you're effectively lending $9.50 to receive $10 in a year, implying an interest rate of about 5.26%.

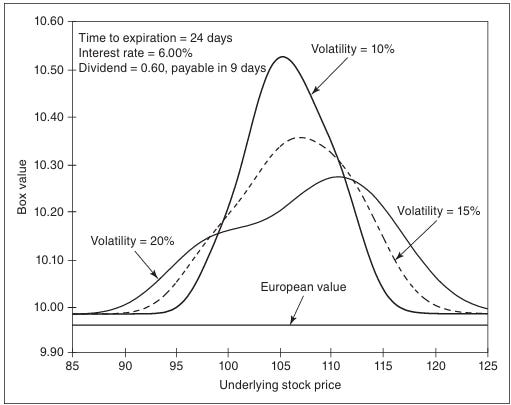

However, as the reader has probably realized, while a European Box is delta-neutral, an American Box is not.

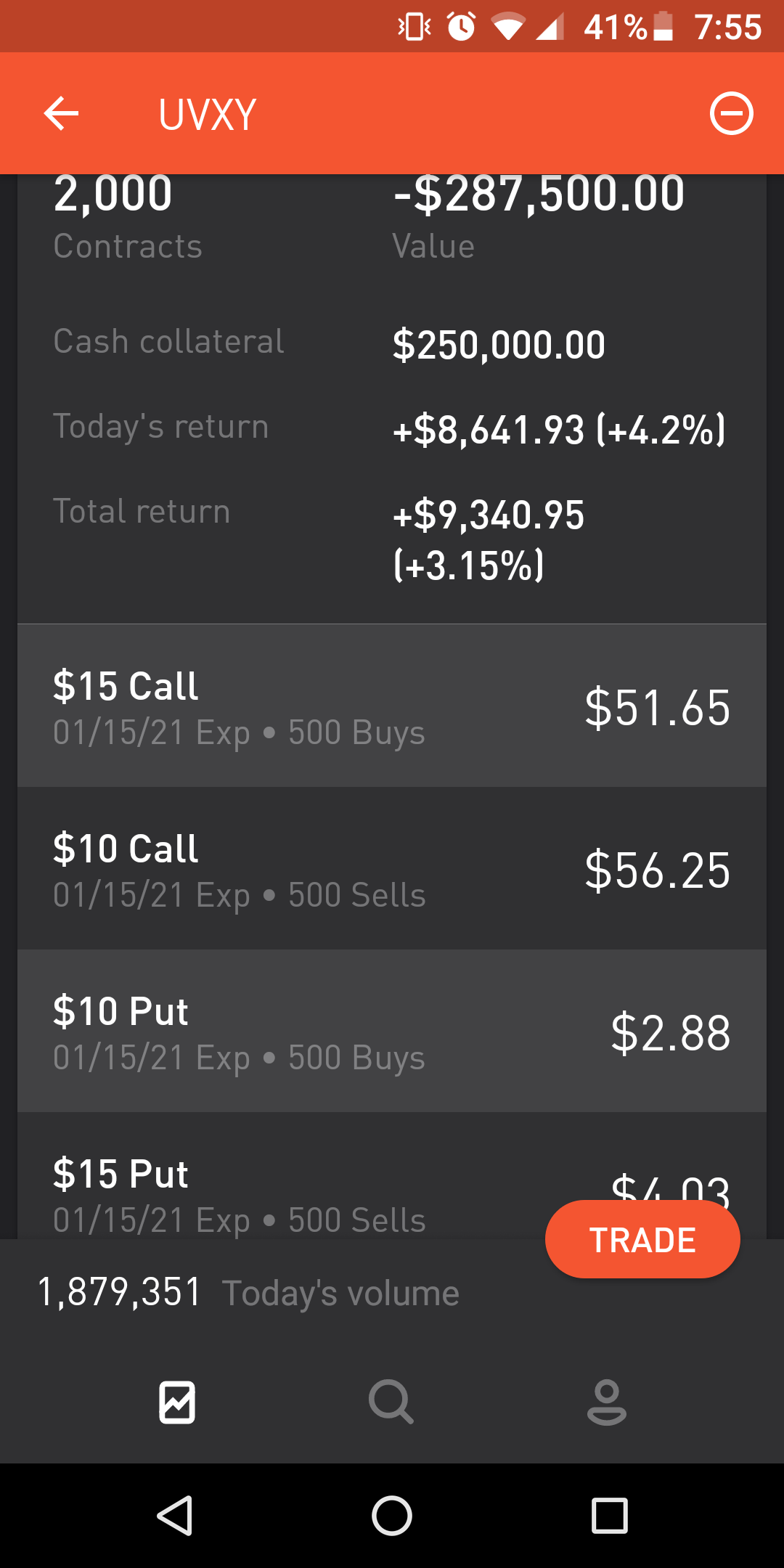

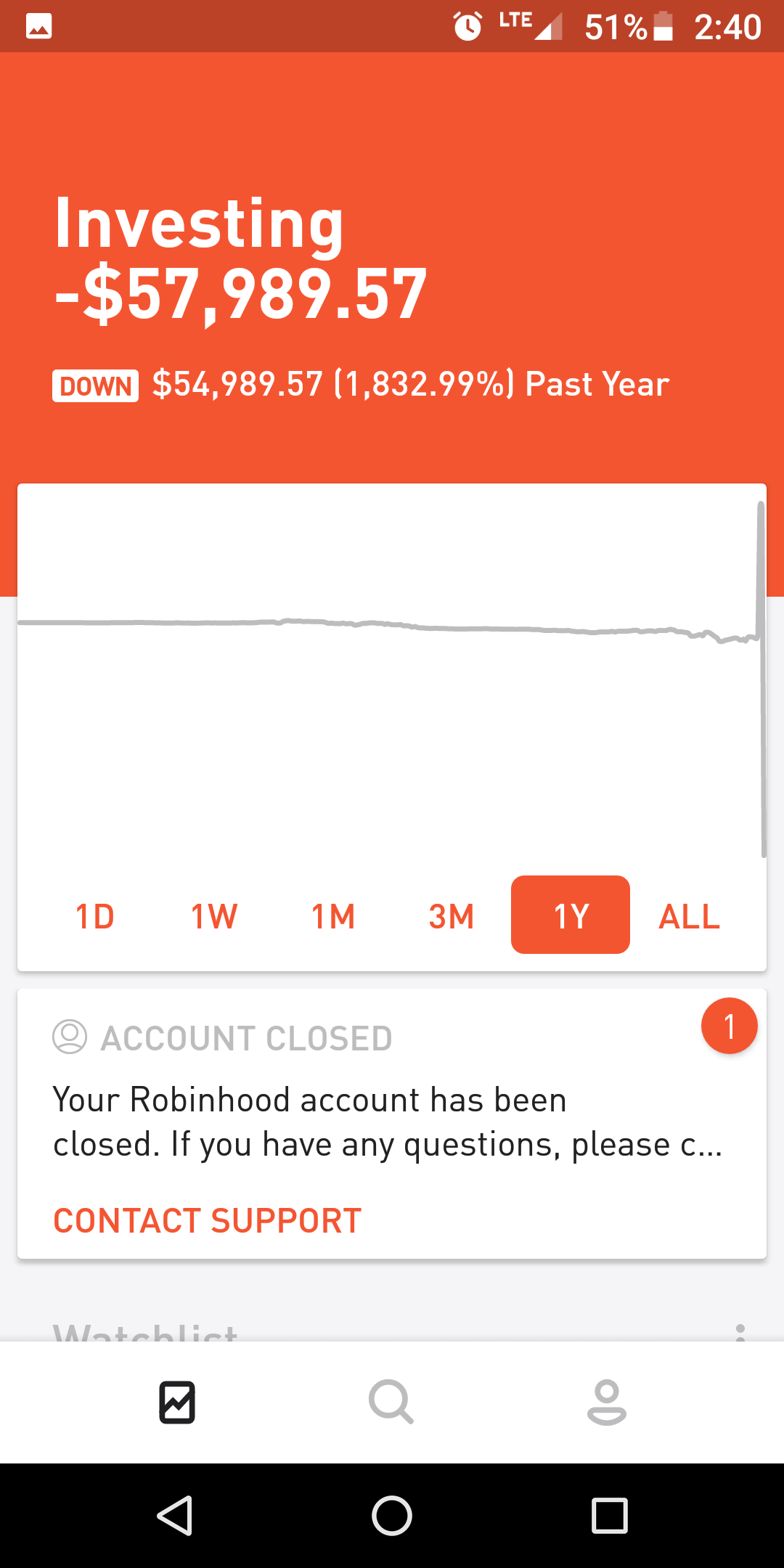

In particular, note that the box’s value is highly sensitive to changes in the underlying. Although by looking at the y-axis, we see that the box deviates from delta neutral only by a small amount, the fact that they are often done in large sizes can result in additional risk. How large was the size for this particular trade? Looking at the beginning of the post, we saw that Robinhood effectively gave 1R0NYMAN a debit of $287,500 on his initial $5,000 investment, which comes to a leverage of 57.5x.

Part of this is 1R0NYMAN misunderstanding how American options work, which is forgivable. However, what is less understandable is how Robinhood risk-management misunderstood how American options worked. 1R0NYMAN, confident in a supposedly "risk-free" trading strategy using box spreads, decided to implement it using Robinhood's platform. Despite lacking sufficient funds, 1R0NYMAN was able to secure a loan of approximately $250,000 from Robinhood against just $5,000 in collateral. This action revealed potential weaknesses in Robinhood's risk assessment protocols as well as their ability to follow regulatory compliance.

Initially, the strategy appeared successful, and Robinhood's algorithms actually indicated profitability. This actually allowed 1R0NYMAN to withdraw $10,000, doubling their initial investment. However, the situation quickly deteriorated when 1R0NYMAN faced obligations of around $60,000 (position marked to market) that they couldn't meet. Realizing the extent of their exposure, Robinhood took swift action by liquidating 1R0NYMAN's account. This decision, while protective of Robinhood's interests, raised questions about the company's risk disclosure practices and their adherence to existing contracts. As a result of the incident, Robinhood decided soon after that it would no longer allow the trading of box spreads.

Disclaimer

The information provided on TheLogbook (the "Substack") is strictly for informational and educational purposes only and should not be considered as investment or financial advice. The author is not a licensed financial advisor or tax professional and is not offering any professional services through this Substack. Investing in financial markets involves substantial risk, including possible loss of principal. Past performance is not indicative of future results. The author makes no representations or warranties about the completeness, accuracy, reliability, suitability, or availability of the information provided.

This Substack may contain links to external websites not affiliated with the author, and the accuracy of information on these sites is not guaranteed. Nothing contained in this Substack constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments. Always seek the advice of a qualified financial advisor before making any investment decisions.