We discuss why on‑chain options have lagged perpetuals, namely, siloed collateral demands and the absence of native leverage incentives; we trace the past waves of on‑chain options innovation, highlight the plumbing breakthroughs, and demonstrate how non-vanilla payoffs can still bootstrap vol‑surface liquidity. We discuss also how recent U.S. legislation and pro‑innovation SEC guidance clear the path for tokenized equities and bonds to enjoy peer‑to‑peer derivatives, eliminating the fee that banks typically charge to issue them, and delivering transparent, programmable, infinitely composable contingent claims.

This post was partially inspired by us reading Trading Optionality; the folks at Decentralized.co know what they are talking about and we heavily recommend anyone interested in staying up to date on happenings in decentralized finance to subscribe to them.

The Case for On-Chain Options

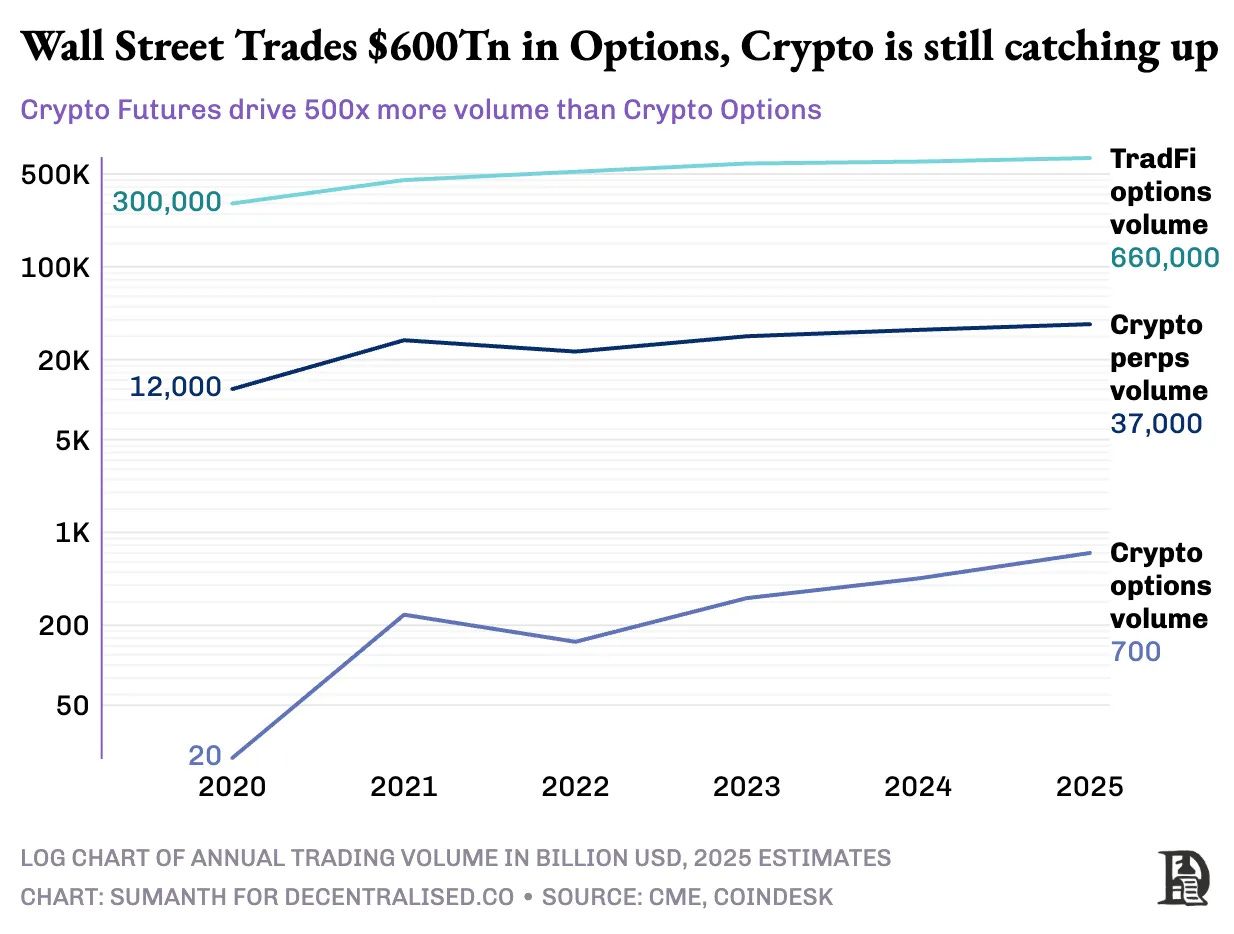

In Trading Optionality, Sumanth Neppalli and Joel John note that while on‑chain perpetuals have become the go‑to leverage toy in crypto, options - despite their recent explosive growth in traditional markets - have barely registered on‑chain.

Two main reasons were given to explain this discrepancy.

First, it was noted that while on‑chain order‑book protocols have tried to replicate centralized exchanges’ cross‑margin benefits, historically they have fallen short. To elaborate, when a desk sells $120K BTC deltas of calls and hedges with $100K BTC-perp deltas, the risk engine should net those positions and asks for margin only on the $20K deltas, freeing up $100 K of collateral for new quotes (ignoring gamma).

However, tokenizing each strike and expiry into its own ERC‑20 silo breaks this: a next‑Friday call can’t recognize the BTC‑perp hedge, so the market maker is forced lock 100% of both legs instead of just the net risk. Since market-making is a low-margin and capital intensive business, the need to overcollateralize each position makes liquidity provision expensive, and hence prevents market formation.

Second, it was noted that options are popular among US retail traders because regulated TradFi markets tightly cap leverage on margin trades (Regulation T limits initial margin on equity purchases to 50%), making options the primary tool for scalable exposure. In other words, people are buying options not for convexity, but for leverage in linear exposures; however, in DeFi it is easy to attain leverage as multiple protocols allow traders to leverage up to 1000x on their positions.

Contrast perpetuals’ seamless, wallet‑to‑wallet custody with the on‑chain options world’s fragmentation and steep learning curve (strike selection, time decay, implied vol, etc…), and one can see why it was hard for options to take off from the demand side. Perpetuals thrived because they bundled every leverage level into a single deep liquidity pool; options, by tokenizing each strike and expiry into its own silo, splintered capital and saddled users, and especially professional market‑makers, with inefficient collateral demands.

In tracing on‑chain options’ three evolutionary phases, the authors’ show how each wave solved some problems only to reveal new ones. First came Opyn’s peer‑to‑peer ERC‑20 tokens, which worked until gas fees dwarfed premiums. Then Hegic’s AMM pools and Lyra’s delta‑hedged vaults promised one‑click UX and off‑chain oracles, but both models buckled under extreme market moves or liquidity droughts. Ribbon’s weekly covered‑call auctions gave depositors yield in bull markets but trapped capital and bled during downturns. Solana‑based CLOB experiments (PsyOptions, Zeta, Drift, Aevo) brought order‑book sophistication and cross‑margining ideas but still suffered from on‑chain gas constraints and sparse quotes.

Looking forward, the authors argue that true on‑chain options are now made possible by improvements to financial plumbing: unified collateral management, atomic execution, real‐time risk engines that view a trader’s entire portfolio as one margin requirement, and deep, composable liquidity across perps and options. They spotlight Hyperliquid’s HyperEVM as the first protocol to deliver this infrastructure‑first vision, combining shared liquidity pools, cross‑margin, and instant liquidations. With traditional market‑makers returning post‑FTX, more battle‑tested chains online, and a growing willingness to blend on‑ and off‑chain components, the stage is set for on‑chain options to finally go mainstream, transitioning from a collection of experiments to a standardized, institutional‑grade ecosystem.

Nonetheless, it was also noted that “If options are to return, it may require a mix of developer talent that understands how the product works, market-maker incentives, and the ability to package these instruments in a way that is retail-friendly. Can there be on-chain options platforms where a few make life-changing sums? After all, that’s what memes offered. It had people dreaming of making seven figures from a few hundred dollars. Meme assets worked as they offered high volatility, but they lacked lindy effects. Options, on the other hand, have Lindy effect and volatility, but are hard for the average individual to understand. We believe there will be a class of consumer apps that focus on bridging this gap.”

Rethinking Optionality On-Chain

In TradFi, retail traders lean on vanilla options primarily because regulated spot and futures leverage is capped; options deliver 20×–50× effective leverage via a small upfront premium. In crypto, where 100× perpetuals are just a click away, classic calls and puts lose their “wow” factor. To excite on‑chain clients, we may need to go beyond plain‑vanilla strikes and expiries, designing payoffs that feel fresh, accessible, and aligned with crypto’s ethos of experimentation.

One way to do this is to look at the rich menu of exotic payoffs and structured products that have thrived in other corners of the world; particularly APAC, where retail investors routinely buy autocallable notes and reverse convertibles despite their complexity because they are accessible (while less so in the US due to regulation).

Yet it’s not enough merely to port APAC structures to crypto wholesale. We need to think about how the underlying market regime shapes demand. Autocallables, for instance, offer attractive coupon yields in low‑growth, low‑yield environments (like those in Korea, China, and Japan) by combining options into a single, wrap‑around product that pays investors a periodic income.

In the U.S., we remain in a persistent high‑growth backdrop, punctuated by sharp rallies in mega‑caps and the occasional meme‑driven squeeze. Here, products that shift expected value to the tails, transforming equity exposure into “lottery tickets”, are perhaps likely to resonate. Lookback options (calls on the maximum price over a period) and rainbow options (calls on the maximum of a basket) let speculators chase the single biggest upside move without committing fully to spot. These may be precisely the kinds of payoffs that can feed chatter and FOMO.

At the same time, the enduring success of covered‑call and buy‑write ETFs suggests that yield‑hungry investors still crave income. Crypto‑native versions of autocallables, perhaps using wrapped Bitcoin or staked ETH as the underlying, with periodic coupon‑like distributions paid in stablecoins, could bridge that gap. Range accrual products, which pay interest only when the asset remains within a defined corridor, might also translate naturally to 24/7 and highly volatile crypto markets.

Moreover, for the crowd that already treats Polymarket or Kalshi like digital sportsbooks, simple binaries or odds‑based payoffs could be the on‑ramp to more sophisticated derivatives (consider parlays on stocks!).

Fundamentally, structured products, and options in general serve three broad purposes: protecting principal, generating income, or delivering leveraged upside. In TradFi, these use cases are mapped onto bond‑like, yield‑focused, or lottery‑style payoffs respectively, each tuned to the prevailing macro regime.

Indeed, if we imagine that most asset returns approximate a bell curve around their long‑term trend, vanilla spot or perp positions tend to deliver roughly normal outcomes centered on the mean. Options let us reshape that distribution. Selling calls or designing range‑accrual structures compresses payoffs toward the center, trading off extreme upside for more consistent, median‑level yield, while buying puts or crafting protective collars reallocates exposure to the left tail, capping losses in severe drawdowns. Conversely, deep out‑of‑the‑money calls, lookback options (calls on the maximum price over time), or digital barrier structures push payoffs into the right tail, creating true “lottery ticket” payoffs that only hit on extreme rallies.

Critically, a truly liquid on‑chain options layer doesn’t depend on retail falling in love with plain‑vanilla calls and puts. What it really needs is for users to embrace some compelling risk‑transformation application, whether that’s a time‑weighted lookback to capture the biggest swing, a one-touch barrier that pays out when volatility spikes, or a range‑accrual that delivers steady yield.

Every time someone trades one of these instruments, they’re implicitly quoting a point on the volatility surface, and a combination of trades forms the basis for the inference of base volatility, skew, curvature, and term structure. In other words, the price of any on‑chain option is a bijection onto the vol surface parameters we care about. As long as your chosen payoff resonates, it will naturally inject liquidity into the corresponding slice of the surface, knitting together depth across strikes and maturities without ever touching a vanilla call.

Modern options markets are really just markets for model parameters, reified via Black–Scholes pricing. I.e. we are trading vol, skew, steepness; not individual options. In TradFi, we’ve historically channeled liquidity into the volatility surface through vanilla calls and puts, because regulation and leverage caps left users no other path. In crypto, with leverage and derivatives plumbing unshackled, any product that cleanly expresses a vol dependency can serve as the on‑ramp. Whether it’s a Euro‑style digital, a barrier‑knock‑in/out, a lookback, or a structured range note, the key is finding the payoff that clicks with user psychology. Once that happens, trading that instrument will bootstrap liquidity not only for itself but for the entire vol surface, turning a single popular product into the backbone of an infinitely customizable, truly liquid on‑chain options ecosystem.

Finally, it is important to note that many of the most enticing exotic payoffs, barrier digitals, autocallables, lookbacks, range accruals, mask very sophisticated risk engines behind a single, easy‑to‑understand “if X happens, you get Y” promise. You don’t need to grasp path‑dependency, volatility clustering, or multi‑asset correlation to see the appeal: “If Ether trades above $4k on expiry, you pocket 20%,” or “Collect a steady 5% coupon as long as Bitcoin stays in this corridor.” By operating in a jurisdictionally agnostic, permissionless layer, untethered from legacy regulations, these intuitively attractive structures become not just feasible but natural first movers for retail-friendly, composable derivatives.

Rethinking Optionality on Real-World Assets

Over the past six months, the U.S. has shifted from “regulation by enforcement” toward clear, innovation‑friendly rules. In January 2025, Executive Order 14178 revoked the outdated 2022 crypto framework (EO 14067) and tasked a new federal working group with designing a digital‑asset regime within 180 days, an explicit signal that Washington wants growth, not gatekeeping. In June, the Senate passed the GENIUS Act, finally carving out stablecoins from securities law and imposing transparent, asset‑backed reserve requirements, opening the door for compliant issuers to scale without legal limbo. And just last week, the House approved a crypto market‑structure bill that expands CFTC authority over digital derivatives, promising clearer rules and less regulatory drag on novel on‑chain products.

More recently, the new SEC chair has signaled a genuine willingness to carve out safe harbors for on‑chain experimentation, publicly weighing staff‑level exemptions for tokenized securities and decentralized derivatives protocols. At the same time, Polymarket’s decision to relaunch in the U.S. under a CFTC‑compliant framework shows that major prediction‑market and exotic‑derivative venues can coexist with regulators, not in spite of them. Taken together, these developments point toward an end state where blockchain technology finally lives up to its promise: real‑world assets, stocks, bonds, real estate shares, are tokenized on a public ledger, and any peer can spin up composable, permissionless derivatives contracts against them.

Such a landscape isn’t just good news for HODLers of ETH or BTC, as it unlocks the same derivatives toolkit for holders of tokenized real‑world assets. Today, retail investors around the world who want structured payoffs on stocks or bonds must go through banks charging roughly a 20 percent “vol‑premium” edge. However, these risk transformation are so attractive that people keep buying them in spite of the premium, to the extend that they create structural dislocations in the market.

For example, see below a real slide that Goldman sends to its institutional partners describe how the products they sell structurally dislocates dividend futures.

Indeed, a big part of the structured derivatives business at any major bank is “risk-recycling” which is a nice way of saying selling over-priced financial products to retail clients and then “recycling” excess risk to hedge fund clients so that the bank has sufficient risk capacity to issue even more financial products. The slides below literally show a pitch for partners to “share risk” with Goldman.

The hidden slippages that banks charge mean that the typical investor is effectively “renting” their risk transformation to Wall Street, handing over a fifth of their potential gains just to play the yield‑seeking or protection‑seeking game. Now, imagine instead a truly free financial system on chain: tokenized equities, bonds, and real‑estate shares live in open markets where any smart‑contract derivative, be it a correlation swap, dividend basket, or barrier digital, can be listed, back‑tested, and traded without middlemen.

Retail participants could take both sides: some selling “lottery‑ticket” upside via deep‑OTM calls or lookback options, others buying steady coupons through range‑accruals or covered‑call mills. No opaque pricing grid, no hidden carry fees, just transparent, peer‑to‑peer risk‑transformation and a genuine increase in utility for every user.

Disclaimer

The information provided on TheLogbook (the "Substack") is strictly for informational and educational purposes only and should not be considered as investment or financial advice. The author is not a licensed financial advisor or tax professional and is not offering any professional services through this Substack. Investing in financial markets involves substantial risk, including possible loss of principal. Past performance is not indicative of future results. The author makes no representations or warranties about the completeness, accuracy, reliability, suitability, or availability of the information provided.

This Substack may contain links to external websites not affiliated with the author, and the accuracy of information on these sites is not guaranteed. Nothing contained in this Substack constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments. Always seek the advice of a qualified financial advisor before making any investment decisions.