Pin Risk

A brief discussion regarding an often underestimated risk.

Option pin risk refers to the potential for options to expire on the strike. The risk is particularly pronounced for option writers who may face assignment if the underlying asset closes at or near the strike price. For example, if a stock closes exactly at the strike price of a heavily traded option, the writer may be uncertain whether they will be assigned or not. This uncertainty can lead to over-hedging or under-hedging, potentially resulting in losses.

While it may seem unlikely that an option can expire exactly at the money, we note that the very act of hedging can pin a stock to its strike as it approaches expiry. In particular, investors who are long gamma can pre-calculate their delta hedges and place them as limit orders on the order book. The trades they place sit on the bid and offer, and therefore pins the underlying to its strike and reduces its volatility.

The amount of hedging activity has to be significant compared to traded volume in order for this to be a real effect, and as such one can expect that illiquid stocks with relatively high option activity from institutional participants (retail doesn’t delta hedge) experience elevated pin risks.

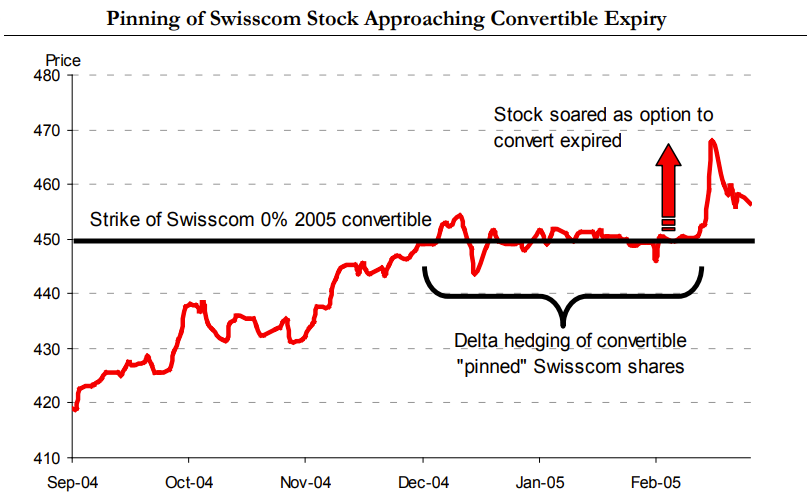

A particularly notable example of hedging activity pinning the stock to its strike can be found in Colin Bennett’s Trading Volatility:

One of the most visible examples of pinning occurred in late 2004/early 2005, due to a large Swiss government debt issue, (Swisscom 0% 2005) convertible into the relatively illiquid Swisscom shares. As the shares traded close to the strike approaching maturity, the upward trend of the stock was broken. Swisscom was pinned for two to three months until the exchangeable expired.

After expiration, the stock snapped back to where it would have been if the upward trend had not been paused. A similar event occurred to AXA in the month preceding the Jun05 expiry, when it was pinned close to €20 despite the broader market rising (after expiry AXA rose 4% in four days).

An observation that one may make is that when market participants are net long volatility, whether through explicit options or instruments with embedded optionality like convertible bonds, their hedging activities tend to suppress realized volatility. The opposite is of course also true, hedging activity when short gamma tends to exacerbate volatility.

As financial markets have become more sophisticated, there has been a significant shift in how these traditional financing instruments are viewed and managed. While instruments like convertible bonds and structured notes were originally designed primarily as funding tools, market participants (i.e. hedge funds) have increasingly recognized and sought to capitalize on their embedded optionality (e.g. in convertible bond arbitrage traders simultaneously hold the convertible bond and short the underlying stock, dynamically adjusting their hedge ratios).

Disclaimer

The information provided on TheLogbook (the "Substack") is strictly for informational and educational purposes only and should not be considered as investment or financial advice. The author is not a licensed financial advisor or tax professional and is not offering any professional services through this Substack. Investing in financial markets involves substantial risk, including possible loss of principal. Past performance is not indicative of future results. The author makes no representations or warranties about the completeness, accuracy, reliability, suitability, or availability of the information provided.

This Substack may contain links to external websites not affiliated with the author, and the accuracy of information on these sites is not guaranteed. Nothing contained in this Substack constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments. Always seek the advice of a qualified financial advisor before making any investment decisions.